Share

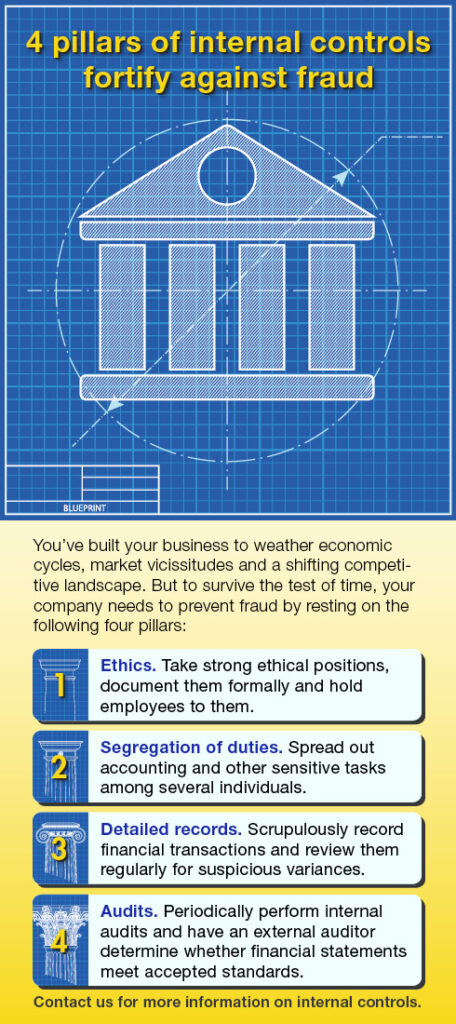

The core of any organization’s fraud-prevention program is strong internal controls. Yet too many organizations either fail to develop controls that address common risks or, if they establish controls, neglect to enforce them. Your organization must do both if it wants to help prevent occupational theft and fraud perpetrated by outsiders. Internal control policies should address both common fraud risks and those specific to your organization.